Payment Authorization Compliance for Collection Agencies: An Operator’s Guide

TABLE OF CONTENTS

Most agencies think about Fair Debt Collection Practices Act (FDCPA) risk as a conversation problem. What agents say, when they call, how the letters read. That’s where the training budget goes, and fair enough. That’s where the statute shows up most visibly.

But there’s a second moment that deserves the same attention: the payment itself.

Here’s the scenario worth designing for. The consumer agreed to pay. The agent did everything right. Then, sixty days later, a dispute arrives over a payment the consumer doesn’t remember authorizing. What happens next comes down to one thing: whether your process captured and stored that authorization well.

One note before we start: I’m not a lawyer, and this isn’t legal advice. This is about payment authorization compliance as workflow.

Payment authorization belongs at the finish line, not buried in the file

The payment moment is the finish line of the collections process. Everything the team did well up to that point, the outreach, the negotiation, the agreement, either becomes a record right there or it doesn’t.

In my experience, agencies know the rules and work hard to follow them. The gap is rarely knowledge or effort. It’s that authorization records often live in places that take real effort to produce on demand. A call recording that takes a day to pull. A notes field. A folder of confirmation letters. The team did the work; the proof just lives in too many places.

And when proof scatters, an honest misunderstanding grows teeth. A consumer sees a debit they forgot agreeing to and calls their bank instead of your office. A question your team could have settled in minutes becomes a dispute. It lands on your client’s brand as much as yours.

What payment authorization compliance actually requires, in plain English

Two rules do most of the work here, and neither requires a law degree to build a workflow around.

First, the FDCPA piece. The rule itself is one sentence long: a collector can only collect amounts expressly authorized by the agreement creating the debt or permitted by law. Convenience fees are the live example, and federal appeals courts have applied that rule to phone and online payment fees as recently as 2025.

The practical takeaway is simple: before charging a fee on any payment channel, know where that fee is authorized. Routing it through a third-party processor doesn’t change the analysis. (Worth knowing: the Consumer Financial Protection Bureau (CFPB) withdrew its 2022 advisory opinion on these fees in 2025, so the safer place to ground the analysis is the statute and the court decisions..)

Second, the Regulation E piece, which matters most on payment plans. This rule is short too: recurring electronic payments, like ACH debits on a settlement plan, need an authorization that’s written or similarly authenticated, and the consumer gets a copy.

“Similarly authenticated” is your friend here. A properly built electronic signature, text confirmation, or web payment flow can satisfy it, which means your payment technology can carry most of this requirement for you.

That’s the core of it. These are documentation standards, and documentation is something you can design for.

The complaint data makes strong records more valuable, not less

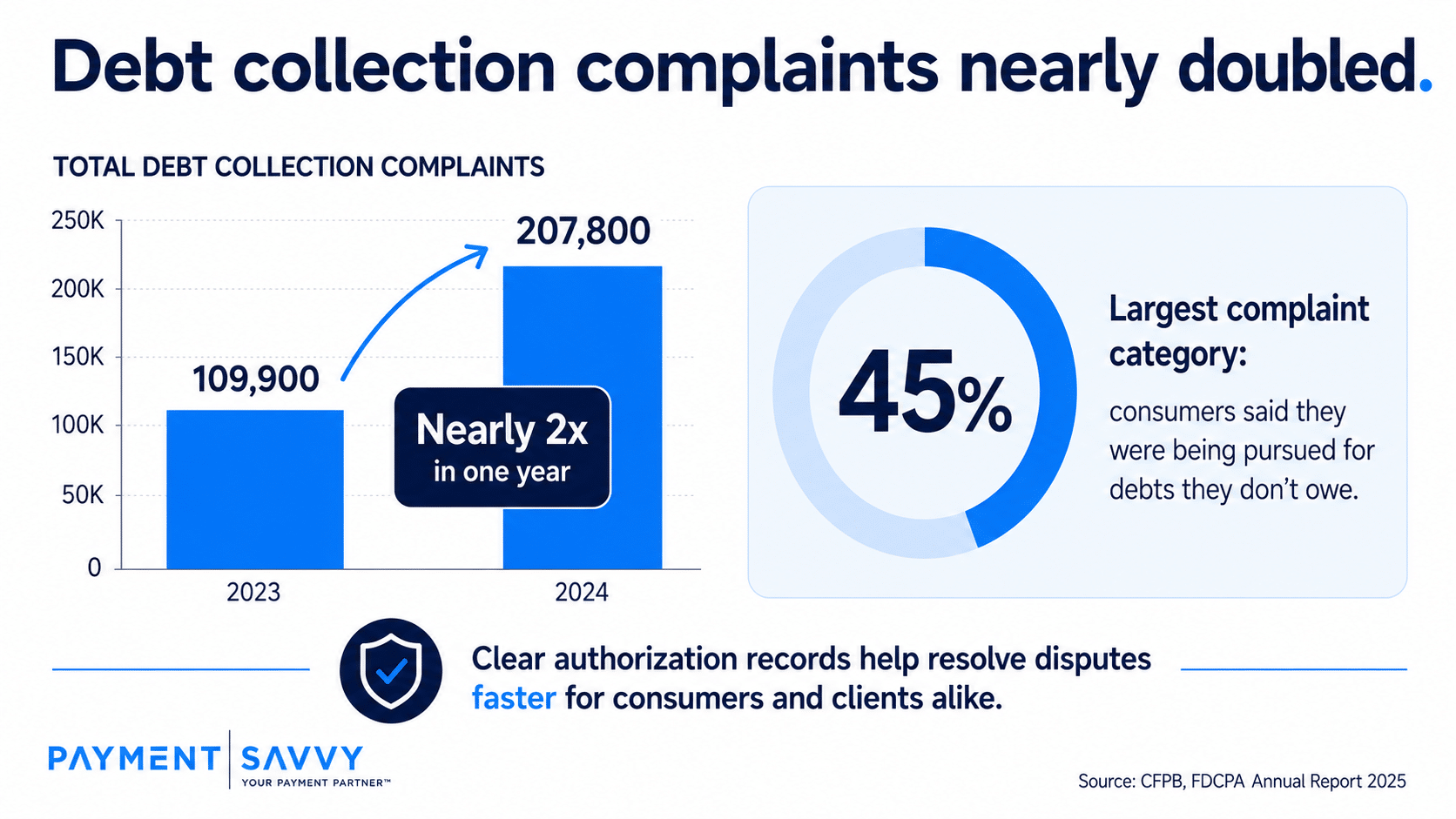

The CFPB received roughly 207,800 debt collection complaints in 2024, nearly double the previous year’s total of about 109,900. The largest single category, at 45%, was consumers saying they were being pursued for debts they don’t owe.

Read that carefully. Consumers have become quicker to question the legitimacy of the whole interaction, not just the balance. When someone sees a payment they don’t remember authorizing, account notes may not be enough. It is solved by producing a clear record of what was authorized, when it was authorized, and how the consumer received confirmation.

CFPB debt collection complaints nearly doubled from 2023 to 2024.

That is where authorization records become more than a compliance checkbox. They give your team a clean way to answer questions before they become escalations, disputes, or complaints.

The operational lesson is simple: the more consumers question, the more important proof becomes. And the best proof is not something your team reconstructs later. It is something your payment workflow captures automatically at the moment the payment is made.

Why strong documentation is a competitive advantage for agencies

When a creditor client asks how authorizations are handled, records beat reassurance. Anyone who’s sat through a client audit or answered the compliance section of an RFP knows the difference between saying “we capture authorization on every plan” and attaching the export that proves it. In this business, a single client relationship can be worth more than a year of margin on a portfolio. Documentation protects that relationship quietly.

There’s also the person on the other side of the payment. A consumer in collections often arrives anxious, primed to expect the worst. A clear confirmation in hand, showing exactly what they agreed to and when, replaces surprise with certainty. That’s good compliance and good customer experience at the same time.

Trust is the product in this industry. Documentation is how you prove it.

What payment authorization compliance looks like day-to-day

The strongest programs I’ve seen share one design principle: the authorization record is a byproduct of taking the payment, not a separate task someone has to remember.

Start with where authorizations are born. When a consumer pays through a web portal, a text-to-pay link, or an IVR flow, the system does the work. It captures, timestamps, and stores the authorization as part of the transaction. When a consumer sets up a plan verbally with an agent, build in an automatic follow-up. A confirmation text or email memorializes the terms without anyone having to remember. The goal is the same in every channel: the record creates itself.

For recurring plans, hold one simple standard. Every plan produces a written or electronically authenticated authorization showing the amount, the schedule, and the account it draws from. The consumer gets a copy without asking. That single habit covers most of your payment authorization compliance surface area under Reg E.

On fees, know your portfolios. Whether a convenience fee is permissible depends on the underlying agreements behind each one. Configure fee settings portfolio by portfolio, and revisit them as new business comes on.

Honor revocations quickly, and log them the way you log authorizations. A consumer who cancels a plan and sees the debits stop immediately is a consumer who trusts the next conversation.

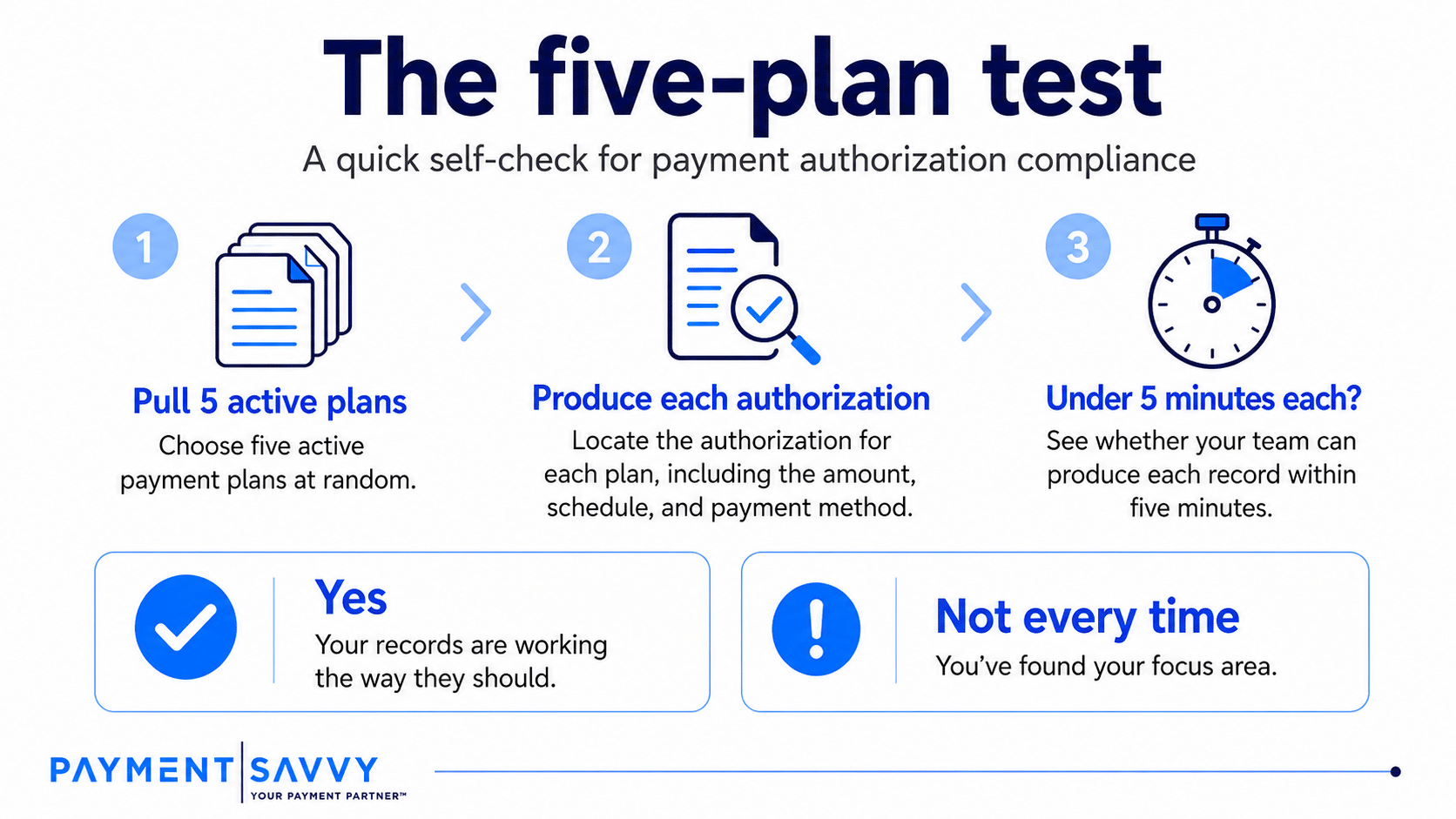

Then give yourself a simple health check I call the five-plan test. Pull five active plans at random and see whether your team can produce each authorization within five minutes. Passing means your records are working the way they should. If a few take longer, you’ve found exactly where to focus. Better yet, you found it on your own schedule, not an auditor’s.

An authorization you can’t produce is an authorization you don’t have.

Compliance you don’t have to remember is compliance that holds

None of this asks your agents to become the compliance layer. It asks your workflow to be. Good people have busy days; well-designed systems don’t.

That’s the lens we bring at Payment Savvy when we work with collection agencies on payment technology: authorization capture, confirmation delivery, and record retention built into the payment channels themselves, across IVR, text, and web, so the documentation exists because the payment happened.

Want a second set of eyes on how your payment stack handles the five-plan test? We’d welcome the conversation.