Chargebacks in Collections Are Getting Pricier. Here’s How Agencies Can Stay Ahead.

TABLE OF CONTENTS

Many chargebacks in collections are not the kind of fraud most people picture.

A consumer makes a payment. Three weeks later, they call their bank and say they do not recognize the charge. The issuer pulls the money back before your team has even gathered the details.

No stolen card. No skimmer. No elaborate scheme.

Just a person who forgot the arrangement, did not recognize the billing descriptor, regretted the payment, or decided the bank felt like a faster path to their money than calling your agency.

That is where chargebacks get messy in collections.

The payment may have been authorized. The debt may be valid. Your team may even have documented the arrangement somewhere. But if that documentation is hard to find, incomplete, or scattered across systems, the dispute gets harder to fight.

And with the Visa Acquirer Monitoring Program, commonly known as VAMP, bringing more attention to dispute and fraud activity, agencies have less room to treat chargebacks as an occasional nuisance.

The takeaway is not panic. It is process.

Chargeback prevention in collections starts with making payments easier for consumers to recognize, easier for your team to document, and easier to defend when a dispute comes through.

Why This Matters Now

Chargebacks have always created operational drag. They pull money back, create fees, and force your team to prove what happened.

Today, the stakes can reach beyond the individual disputed payment.

Card networks continue to watch dispute and fraud activity closely. The VAMP framework may evaluate activity at different levels, including aggregated merchant or sponsored merchant levels, and may require remediation tools or technologies when unusual activity shows up. Mastercard also references merchants reported under its Excessive Chargeback Program in its public rules.

For collection agencies, the important point is simple: chargebacks are not just an accounting issue. They can become a processing issue.

A few disputes may not seem alarming on their own. But if activity builds across a merchant account, portfolio, channel, or workflow, it can create pressure faster than leadership expects.

That does not mean every agency is suddenly at risk. It means payment hygiene now carries more operational weight.

Chargeback prevention helps protect cash flow, merchant account stability, and your agency’s ability to keep accepting payments without interruption.

Why Collection Payments Need a Cleaner Trail

Collection payments carry context most transactions do not.

A consumer may remember the original creditor, but not the agency collecting on the account. They may agree to a payment plan over the phone, then forget the timing. They may recognize the debt, but not the billing descriptor on their statement.

Sometimes the dispute is confusion. Sometimes it is regret. Sometimes it is first-party misuse, often called friendly fraud, where a cardholder authorizes a transaction and disputes it later anyway.

For your agency, the result lands the same way every time.

The consumer challenges the payment. The issuer pulls the funds back. Your team has to prove the transaction was valid.

That proof is where many agencies get exposed.

A dispute arrives and the authorization record is buried in call notes. The receipt is hard to locate. The payment plan terms live in one system, while transaction details live in another.

When the response window is already moving, that gap matters.

The strongest agencies do not wait until a dispute arrives to figure out what happened. They build payment processes that create a clear trail from the start.

The payment is recognizable. The authorization is documented. The confirmation is specific. The support path is easy to find.

And when a dispute comes through, the team responds from records instead of memory.

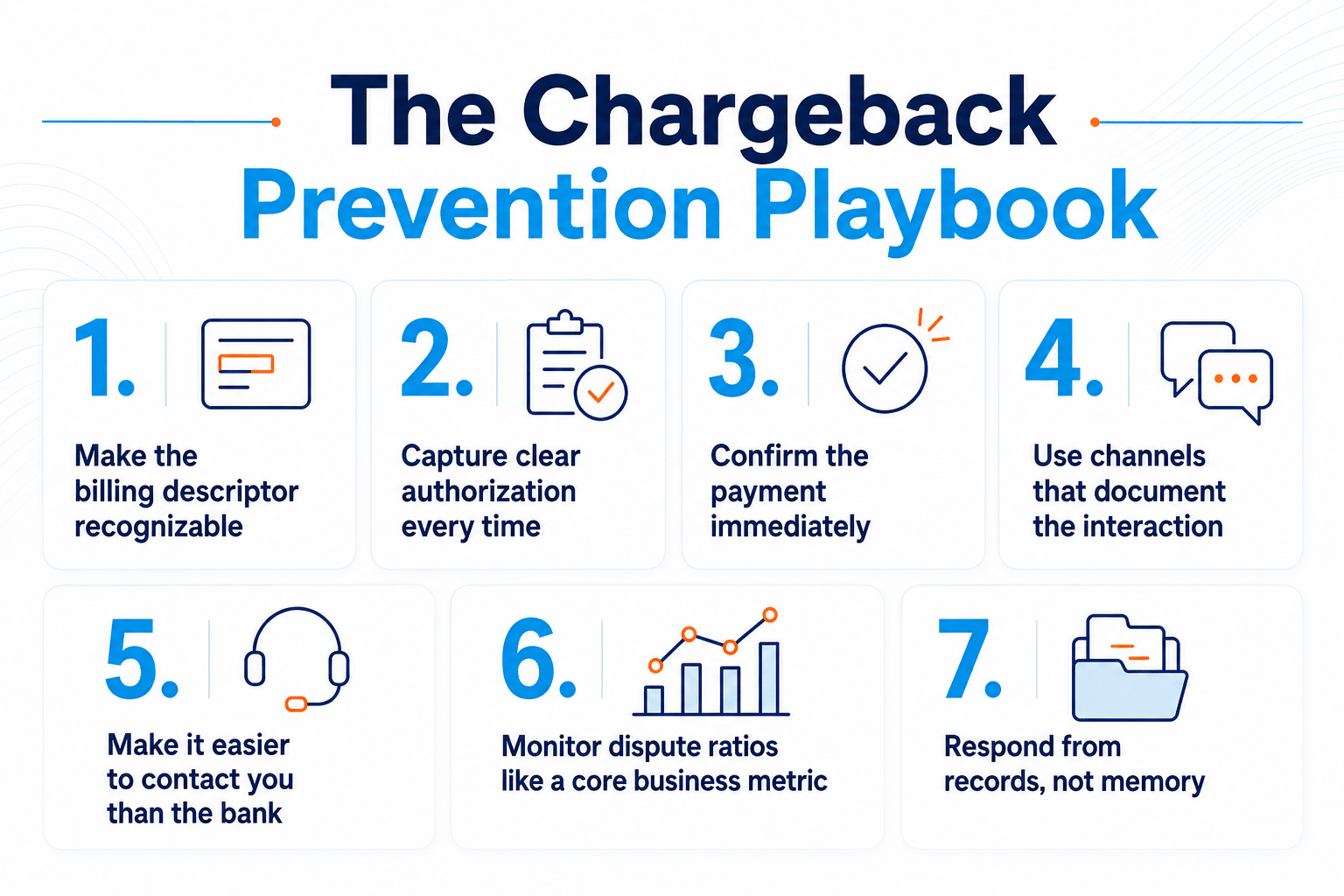

The Chargeback in Collections Prevention Playbook

1. Make the billing descriptor recognizable

If the consumer cannot place the name on their statement, you have already created an avoidable dispute.

A strong descriptor connects clearly back to your agency, the creditor, or the payment experience the consumer remembers. When possible, include a recognizable name or support number that helps the consumer identify the charge quickly.

A confusing descriptor can turn a valid payment into an “I don’t recognize this” dispute before your team gets the chance to explain it.

2. Capture clear authorization every time

Every payment needs a retrievable record of consent. Recurring arrangements need even more care.

Your team should be able to answer a few basic questions quickly:

- Who authorized the payment?

- When did they authorize it?

- What amount did they agree to?

- What schedule did they accept?

- What channel did the authorization come through?

- Were the terms confirmed back to the consumer?

If those answers live in scattered notes, old recordings, or someone’s memory, your response will be weak. Strong authorization records are timestamped, easy to access, and tied directly to the transaction.

3. Confirm the payment immediately

Receipts are not just a courtesy. They are part of the evidence trail.

A clear confirmation by email, text, or on-screen receipt helps the consumer remember what they agreed to and gives your team documentation to point back to later.

Keep the confirmation simple and specific: amount, date, payment method, agency name, and contact information.

A consumer who can recognize and verify the payment is less likely to dispute it out of confusion. And if they do, your team is not starting from scratch.

4. Use channels that document the interaction

Self-service payment channels do more than make paying easier. Digital wallets, IVR, and pay-by-text can create a cleaner record of what happened. They capture the consumer’s action, timestamp the transaction, confirm the amount, and reduce reliance on manual over-the-phone card entry.

That matters in collections. Your team does not just need payment volume. You need payment records that can defend themselves.

When the payment experience documents itself by default, your collectors do not have to remember every detail or rebuild the proof later. The channel does that quiet work for them.

5. Make it easier to contact you than the bank

Some consumers dispute because they do not know who to call. Others dispute because reaching the bank feels easier than reaching the agency.

Put clear contact information on every payment confirmation. Make support easy to find on consumer-facing payment pages. Give consumers a clear path to ask questions or verify a charge before they turn to their card issuer.

You cannot control every decision a consumer makes. But you can remove the friction that pushes them toward the bank first.

6. Monitor dispute ratios like a core business metric

Agencies already track liquidation, payment volume, placements, promises, and collector activity. Chargeback ratios deserve the same attention.

A rising dispute rate is an early warning sign. If your processor or acquirer raises the concern first, your agency is already reacting.

Where possible, look at disputes by merchant account, creditor, channel, workflow, and transaction type. Do disputes cluster around a descriptor? A portfolio? Recurring payment plans? A specific payment method?

You cannot fix what you do not measure.

7. Respond from records, not memory

When a dispute arrives, the question is simple: can you produce the proof?

The agencies in the strongest position are not scrambling through call notes or asking someone what they remember. They already have the authorization trail, receipt, transaction details, and communication history ready to go.

That will not guarantee every chargeback gets reversed. But it gives your team a real response instead of a best guess.

The goal is not perfection. It is to prevent the disputes you can and defend the ones you cannot.

What Good Looks Like for Chargebacks in Collections

A strong chargeback prevention process makes the payment recognizable, captures authorization clearly, confirms the transaction immediately, and builds a digital trail without piling extra work on your team.

It also gives leadership visibility into dispute trends before those trends become processor problems.

That is the difference between payment processing that simply runs transactions and payment infrastructure built for collections.

Where the Right Payment Partner Fits

Most agencies do not need more manual work.

They need a payment setup that creates better records automatically.

That is where the right payment partner earns its keep.

Chargeback prevention depends on how your processing is built: billing descriptors, authorization capture, confirmation flows, recurring payment documentation, reporting visibility, and self-service channels that create an evidence trail by default.

Payment Savvy works with collections and ARM operations specifically, so we do not treat these details like edge cases.

They are the workflow.

From recognizable descriptors and documented recurring authorizations to digital wallets, IVR, and pay-by-text options, the goal is simple: help agencies accept payments in a way that is easier for consumers to recognize and easier for agencies to defend.

Because in collections, the gap between a manageable dispute rate and a merchant account problem often comes down to process.

And process is something you can improve.

The Bottom Line

Chargebacks in collections may feel inevitable, and some are.

But many are not sophisticated fraud at all. They are forgotten payments, confusing descriptors, undocumented authorizations, missing receipts, and payment experiences that leave too much room for dispute.

Those are process gaps. And process gaps can be closed.

As card networks continue to scrutinize dispute activity, agencies cannot afford to treat chargebacks as an occasional nuisance. Payment hygiene belongs in core operations.

Get it right, and you protect more revenue, reduce preventable disputes, and keep your processing relationships stable.

Get it wrong, and you may find out the hard way, one disputed payment at a time.