Convenience Fees for Collection Agencies: What Owners Need to Know in 2026

TABLE OF CONTENTS

Convenience fees look simple from the outside.

Add a few dollars for the convenience of paying online or by phone. Disclose it before the payment goes through. Let the consumer choose whether that channel is worth the fee.

In collections, it is not that simple. That is why convenience fees for collection agencies deserve more than a quick checkout setting or a one-size-fits-all processor answer.

Convenience fees sit in one of the most carefully watched areas of how agencies collect payments. The issue is not just whether the fee is disclosed. It is not just whether the consumer opted in. And it is not just whether the processor can technically support it.

There are two rulebooks in play.

The first is the card-network rulebook. Visa and Mastercard care about how you structure, disclose, and process the fee. The second is the debt-collection rulebook. The FDCPA asks a different question: whether the agency can collect the fee at all.

Those two questions are related, but they are not the same. You can build a fee correctly from a card-network perspective and still raise legal questions under debt collection law.

Before we go any further, a quick but important note: this is an operational overview, not legal advice. Convenience fee decisions depend on your contracts, your account type, your state law, your client requirements, and your agency’s specific compliance posture. Your attorney should be the one to tell you whether and how a convenience fee program applies to your agency.

What follows is the landscape every collection agency owner should understand well enough to ask the right questions.

The card networks care about how the fee is built

Start with the layer most processors talk about first: the card-network rules.

Under Visa’s convenience fee requirements, the fee has to tie to a genuine alternative payment channel. You can’t simply charge it because the consumer used a card. It has to cover the convenience of using a payment channel outside the merchant’s customary method, such as paying online or by phone when you offer that as an alternative.

Visa’s rules also require you to disclose the fee clearly before the transaction completes, and the consumer has to have the opportunity to cancel once they see it.

A convenience fee also cannot be charged in addition to a surcharge. The two are not interchangeable, and they should not be stacked on the same transaction.

This is where terminology matters. A surcharge generally reflects the cost of accepting a card. A convenience fee reflects the convenience of using an alternative payment channel. Those may sound similar in a consumer conversation, but the card networks treat them differently.

That distinction matters even more in collections, where you need to understand, disclose, document, and support every fee.

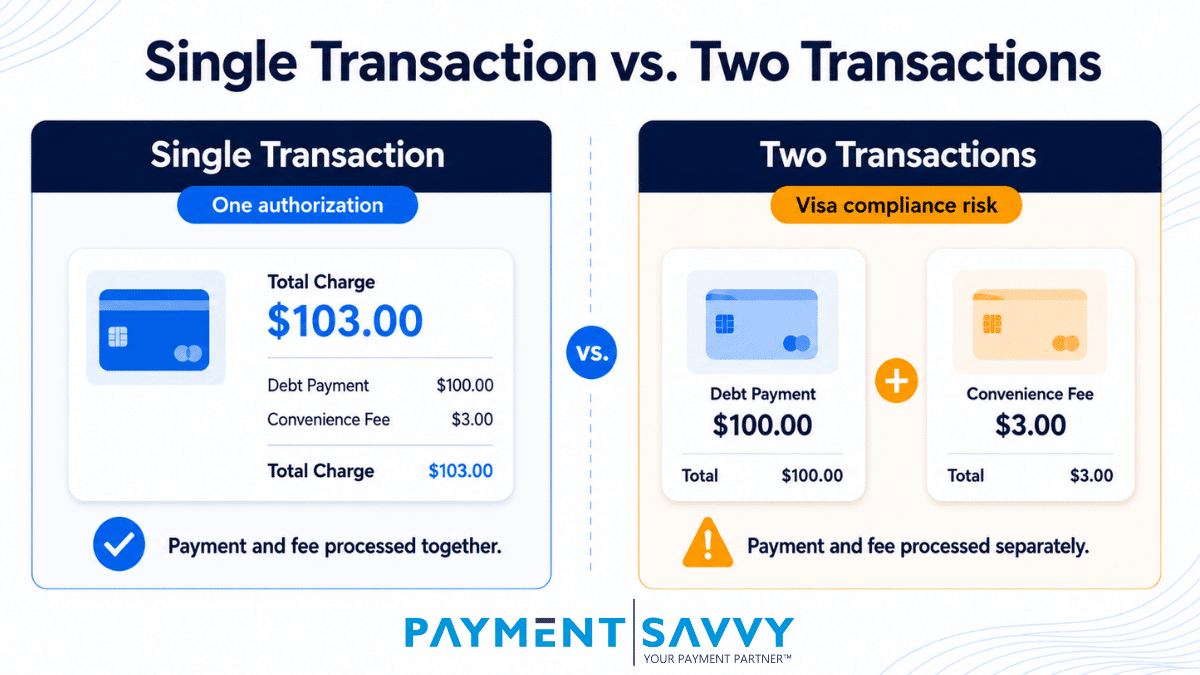

The single-transaction requirement is not a small detail

Now we get to the part collection agencies should pay close attention to.

For Visa convenience fees, the fee must be included as part of the total transaction amount and not collected separately.

That means one authorization. One transaction. The payment and the convenience fee together.

Some payment setups do not work this way. They run the debt payment as one transaction and the convenience fee as a second, separate transaction. That may look clean on a statement. It may even feel easier to explain. But it’s worth understanding how your processor structures it, because the card networks treat the single-transaction approach as the standard.

For any agency evaluating a convenience fee program, this is one of the most important processor questions to ask: does the convenience fee process as part of the same transaction as the payment, or is it run as a separate transaction?

Your processor should give you a clear answer in writing, not language you have to decode.

At Payment Savvy, our convenience fee approach is built around single-transaction processing. The payment and the convenience fee are processed together as one transaction, not split into two separate charges.

That does not answer every legal question for an agency. It does address one of the most important card-network mechanics questions. And in this space, getting the mechanics right matters.

The second rulebook: federal debt collection law

This is where collections differs from many other industries that charge convenience fees.

The FDCPA includes a provision that prohibits a debt collector from collecting any amount, including a fee, charge, or expense incidental to the principal obligation, unless that amount is expressly authorized by the agreement creating the debt or permitted by law.

That is the heart of the issue.

The question is not only, “Did the consumer agree to pay the fee at checkout?” The harder question is, “Was the fee authorized by the underlying agreement or permitted by law in the first place?”

This is an area regulators and courts have paid attention to, and the guidance around it has shifted over time. The specifics are exactly the kind of thing your counsel should weigh for your agency. The durable point for an operator is simpler: authorization matters, and it’s worth confirming before a fee is ever charged.

This is not an area for assumptions

Convenience fees in collections have drawn litigation, and the outcomes have not produced one clean, nationwide answer. The facts matter, including whether a fee-free payment option was clearly available and how the payment was structured. The takeaway for an operator isn’t to predict how a court would rule. It’s to recognize that this is a watched area and to keep your own house in order.

The safest operational takeaway is simple. If your agency charges a convenience fee, you should be able to explain and document three things: where the fee is authorized, how the fee is disclosed, and how the payment is processed.

If any one of those answers is unclear, it is worth slowing down before the fee reaches a consumer.

Why “single transaction” and “separate transaction” can create confusion

This is where the conversation can get frustrating, because different people may use the word “separate” to mean different things.

From a card-network perspective, the convenience fee should run together with the payment as one transaction, not as a separate card charge.

From a legal perspective, some arguments around convenience fees have focused on whether the fee is part of collecting the debt or whether it is tied to a separate optional payment service.

Those are not the same thing.

An agency may need the card payment and convenience fee to process together as one transaction for card-network purposes, while still working with counsel to determine whether the fee is properly authorized, disclosed, and structured from an FDCPA perspective.

That is why processor design and legal review both matter. Your processor can answer how the transaction is built. Your attorney should answer whether your agency can charge the fee. You need both answers before you are comfortable.

The 2026 backdrop: stay disciplined either way

The regulatory environment around these fees has shifted over the years, and it may keep shifting. It’s tempting to read a quieter moment as a sign the issue has cooled.

We’d just encourage agencies not to relax their discipline based on the mood of the moment. Rules and interpretations change. The fundamentals of a defensible program don’t.

When the landscape is unsettled, the agencies in the strongest position are usually the ones with clear documentation, consistent disclosures, fee-free payment options, and a processor that can explain exactly how the transaction is handled.

What disciplined practice looks like

Don’t treat convenience fees like a checkout setting someone toggles on and forgets.

A disciplined program starts with authorization. Before you charge a fee, your agency should be able to point to the agreement, law, or legal basis that supports it.

Next, keep the disclosure clear. The consumer should understand the amount of the fee, why it applies, and that it lands before the transaction completes.

The payment flow should also make fee-free options easy to find. Offering a no-cost way to pay is not only better consumer experience. It has also shown up in litigation as an important fact courts may consider.

Then there is the processing itself. For card-network mechanics, confirm whether your processor runs the convenience fee as part of the same transaction as the payment. If they split the fee into a second card transaction, ask more questions.

Finally, document everything. Authorization basis. Disclosure language. Consumer opt-in. Fee-free alternatives. Processor confirmation. Transaction structure.

If the fee is challenged later, you do not want to rebuild your reasoning from memory. You want the file to already exist.

Where Payment Savvy fits

Payment Savvy works with collection agencies every day, so we know convenience fees are not just a pricing question. They are an operations question, a compliance question, a consumer experience question, and a processor-fit question.

With convenience fees for collection agencies, processor design is only one piece of the conversation. Agencies also need clear authorization, strong disclosures, fee-free options, and documentation they can stand behind. We cannot give your agency a legal opinion. Your counsel owns that. What we can do is help you understand how your payment setup is working at the transaction level.

For agencies that choose to offer convenience fees, Payment Savvy supports single-transaction convenience fee processing. That means the payment and the convenience fee are processed together as one transaction, rather than split into two separate charges.

That matters because processor mechanics are one of the pieces agencies need to get right. The other piece is authorization. That belongs with your attorney.

When you handle both sides of the conversation carefully, your agency can offer convenient payment options without treating compliance as an afterthought.

The bottom line

Convenience fees for collection agencies should not be treated like a checkbox.

They sit between two rulebooks: card-network requirements that govern how the fee is processed, and debt-collection law that governs whether the fee is authorized.

The practical path is not complicated, but it does require discipline. Confirm the fee is authorized. Disclose it clearly. Keep fee-free payment options available. Document the consumer’s choice. And make sure your processor handles the fee as part of a single transaction, not as a separate charge.

That is how a convenience fee becomes what it should be: a transparent payment option, not a liability waiting to surface.

If you are not sure how your current processor handles convenience fees, Payment Savvy can help you review the transaction flow and understand what is happening behind the scenes.