What to Look for in a Collections Payment Vendor

TABLE OF CONTENTS

Nobody starts shopping for a collections payment vendor because they want to.

They start because something stopped working.

A support call went nowhere. A statement didn’t reconcile. An integration looked great in the demo but never really came to life after signing.

Before long, they’re back in another vendor conversation — not chasing something shiny, but trying to fix a setup that has already made the work harder than it should be.

That’s what makes the decision tricky.

In a demo, most platforms look polished. The features sound familiar. The rep has the right answers ready. So buyers naturally compare what’s easiest to compare: price, features, and surface-level functionality.

But the things that usually decide whether the partnership actually works are harder to see up front.

The right collections payment vendor is rarely the one with the slickest demo. It’s the one that holds up after the contract is signed.

That usually comes down to a few things that do not live neatly on a feature grid, and all of them matter more than most buyers realize at the start.

A team that answers

Every processor says they have great support.

Dedicated support. White-glove service. A team that cares.

The words sound good in a sales deck, but they do not mean much until something breaks. That is when you find out what kind of vendor you actually chose.

Ask what happens when payments are failing at 9 a.m. on a Monday and your call volume is already high. Do you reach someone who knows your account, or do you open a ticket and wait? Do you get a real answer, or a polite confirmation that someone will “look into it”?

In collections, the payment is the finish line. When the payment experience breaks, revenue does not post. Your team loses time. The consumer who was ready to pay may not come back and try again later.

That is why the right collections payment vendor cannot just offer support. They need to respond quickly when payment issues are affecting your business.

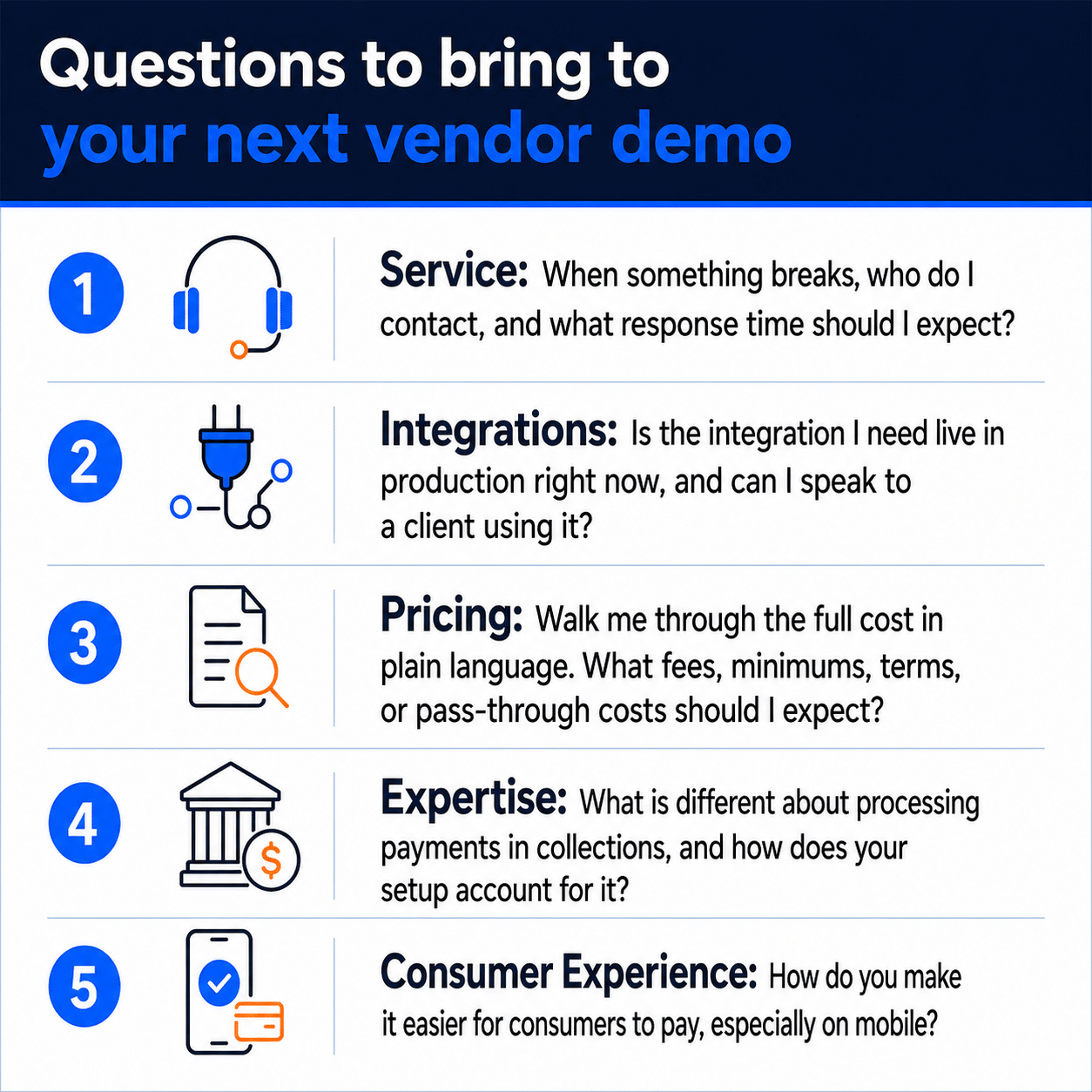

Ask: When something breaks, who do I contact, and what response time should I expect?

Integrations that work in the real world

This is where a vague yes can get expensive.

You ask if the platform connects to your collection management system. The vendor says yes.

But “yes” can mean very different things.

Sometimes it means the integration is live, tested, and already being used by agencies like yours. Other times, it means it could be built with development time, testing, and patience.

Those are not the same thing.

A live integration helps payments post back to your collection management system without your team chasing files, fixing batches, or wondering whether the update went through.

That matters because collectors need to trust what they see when they open an account. If payment activity is delayed, missing, or handled outside the normal workflow, adoption gets harder and follow-up gets messy.

If the integration is still on the roadmap, be clear about what that means. You are not just choosing a payment vendor. You are also taking on a project.

Before you sign, ask what is live today, who is using it, what data moves between systems, how quickly it updates, and what still has to be handled manually.

Ask: Is the integration I need live in production right now, and can I speak to a client using it?

Clear pricing, clear expectations

Payments pricing has a long history of being harder to read than it should be.

Tiered rates. Add-on fees. Pass-through costs. Statements that seem simple during the sales process and much less simple once billing begins.

Confusing pricing is rarely just a billing issue. It is often an early sign of what the relationship will feel like after you sign.

A good collections payment vendor will walk through the full cost in plain language: monthly fees, transaction costs, add-ons, minimums, pass-through costs, cancellation terms, and anything else that may show up later.

The goal is not just to find the lowest rate. It is to understand what you are agreeing to, what may change over time, and what your agency should expect once payments are actually running.

Ask: Walk me through the full cost in plain language. What fees, minimums, terms, or pass-through costs should I expect?

A payment partner who knows collections

Any processor can move a transaction. That is not the differentiator.

The difference is whether they understand the business you are in.

Collections has rules, workflows, and pressure points that general merchant-services providers may not fully understand. Convenience fees have to be handled carefully. Client requirements can vary. Attorneys may have specific expectations. Some accounts come with added scrutiny. And when payment acceptance is at risk, a generic answer is not enough.

A collections payment vendor should already know where the friction lives. They should understand why your team cares about posting speed, consumer payment choice, recurring options, fee handling, integration behavior, and support access.

They should ask about your workflow, your client mix, your compliance exposure, and the moments where payments tend to break down.

When your payment partner knows collections, you spend less time explaining your business and more time running it. That is not a nice-to-have. It is one of the main reasons to choose a specialized partner in the first place.

Ask: What is different about processing payments in collections, and how does your setup account for it?

Make it easier for people to pay

Your collections payment vendor doesn’t just shape your team’s day. It shapes how the person on the other end experiences the moment they pay, and that experience can decide whether the money actually lands.

The shift in how people pay is hard to ignore. The Federal Reserve’s 2025 Diary of Consumer Payment Choice found that U.S. consumers made an average of eleven mobile-phone payments per month in 2024, up from four in 2018. Among adults aged 18 to 24, mobile phones accounted for 45% of all payments.

The human side matters too. PayNearMe research found that 51% of loan-paying consumers said managing and paying loans causes anxiety, while 47% said digital reminders make bill payments easier.

For collections, the takeaway is simple: when someone is ready to resolve a balance, the path to payment needs to be easy. Mobile-friendly options, clear reminders, simple steps, and fewer points of friction can all help move the payment forward.

The right collections payment vendor makes paying easier for your team and for the people you are trying to collect from. Both sides matter.

Ask better questions before you sign

You do not need a forty-line RFP to spot the difference between a polished demo and a partner that can actually support your agency. A few direct questions can tell you a lot.

Pick a partner you can count on

A payment vendor is not just a line item in your budget. It is a partner your team depends on every day and a part of the experience consumers meet every time they pay.

Six months from now, the feature lists will start to blur together. What you’ll remember is whether the people behind the platform picked up when it mattered, connected to your systems without turning onboarding into a project, told you the truth about costs and limits, and understood the business you’re actually in.

Get the fundamentals right, and the rest gets a lot easier.

Payment Savvy is built around that standard: payment setups shaped around how your agency really works, real people who answer when you need help, clear conversations about cost, and a team that knows where collections payment friction tends to show up — for your staff and for the people trying to pay.

If you are weighing your options, we would welcome the conversation.