Meeting Consumers Where They Pay: The Case for Digital Wallets in Collections

TABLE OF CONTENTS

For most of the last decade, the collections industry has invested heavily in modernizing the front end of the consumer journey — better outreach, smarter segmentation, more empathetic messaging, AI-assisted conversations. That investment has paid off. Real results, measurable shifts, things that would’ve seemed impossible ten years ago.

But here’s what hasn’t kept pace: the actual payment moment.

When a consumer is finally ready to resolve a balance — when they’ve clicked the link, weighed the offer, decided to act — the experience they encounter often looks exactly the way it did in 2015. A form. A card number. A billing address. A captcha. Sometimes a redirect to a separate processor. And then, occasionally, nothing — because somewhere between intent and completion, the moment slipped.

Digital wallets are how consumers solve this everywhere else in their lives. The question is whether collections is ready to meet them where they already pay.

The consumer behavior shift is already here

The change isn’t subtle. And it’s not waiting on the collections industry to catch up.

In retail, transit, food delivery, ride-sharing, and peer-to-peer transfers, consumers have been conditioned to expect a tap-to-pay experience. They don’t think about whether a wallet is available — they assume it is. KUBRA’s 2025 Digital Wallets Research found that 61% of consumers already use digital wallets for everyday purchases, and 42% now use them specifically for bill payments — a number that has more than doubled since their 2022 benchmark. The gap between wallet use in daily commerce and wallet use in bill pay is closing fast, and most collection agencies aren’t ready for it.

It’s also worth noting that this shift isn’t purely generational in the way some critics suggest. Wallet adoption does skew younger, but it’s not exclusive to younger consumers. Stripe’s 2025 global holdback experiment, conducted across more than $1.4 trillion in annual transaction volume, found that businesses offering Apple Pay alone saw an average 22.3 percent lift in conversion across eligible checkouts. Baymard Institute’s research consistently finds that stores enabling wallets see a 20 to 26 percent reduction in mobile-specific cart abandonment.

The point isn’t that wallets are the future of payments. The point is that wallets are how a meaningful and growing share of consumers already prefer to pay — and collections, as an industry, has been slower than most to enable them.

What digital wallets actually do behind the scenes

When a consumer taps Apple Pay or Google Pay, what looks simple on the surface is operationally meaningful underneath.

Wallets use tokenized payment credentials rather than the raw card number a consumer would otherwise type into a form. Authentication happens through the device — Face ID, Touch ID, a passcode — rather than relying on the consumer to recall a billing zip code or locate a security code on the back of a card. That combination changes the risk profile of the transaction in ways that matter specifically to collections.

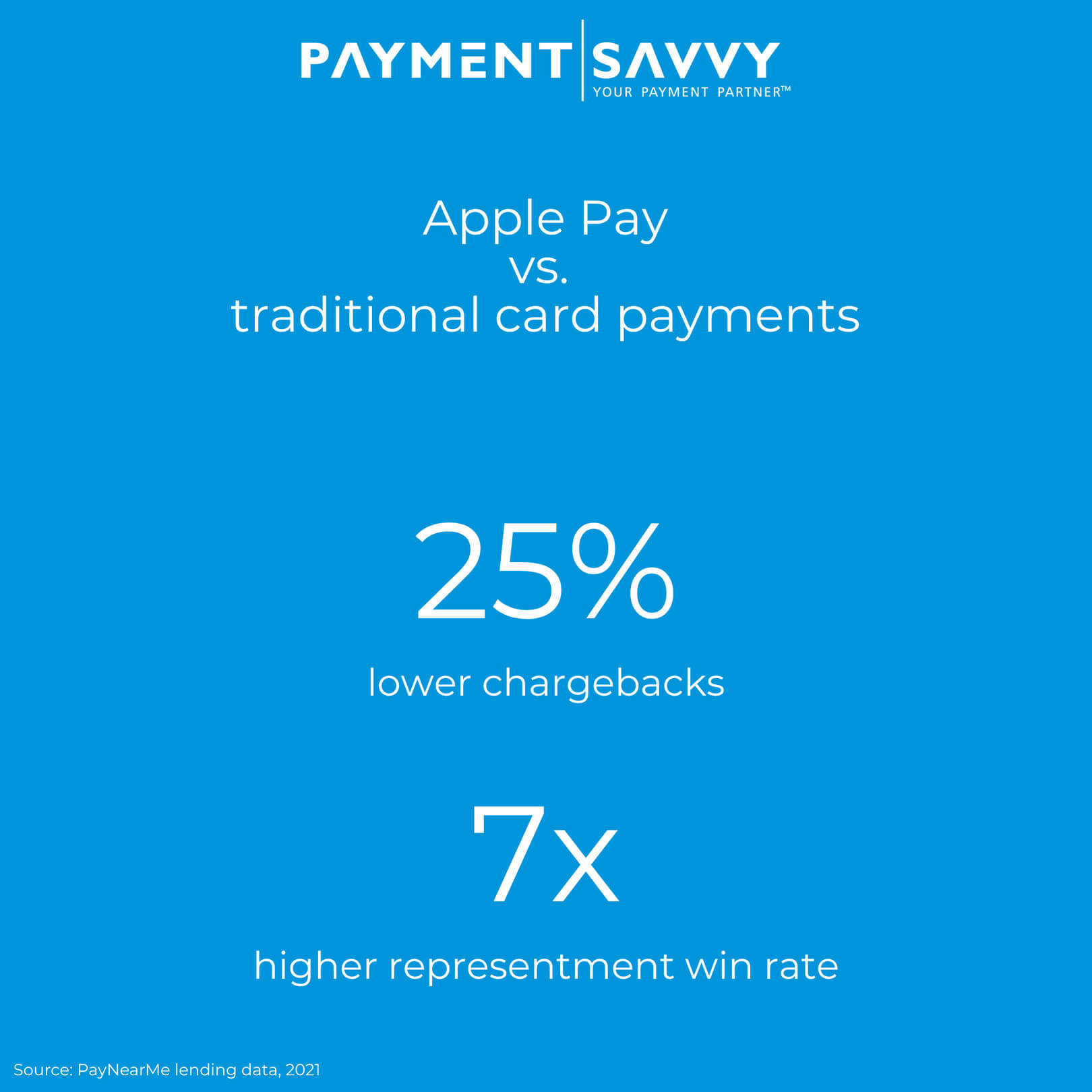

PayNearMe published lending data showing that Apple Pay transactions chargeback 25% less often than traditional card payments, and that merchants won 7 times more chargebacks on Apple Pay disputes than on disputes for other card transactions. The biometric authentication and the cleaner transaction record together make it significantly harder for a consumer to credibly claim the charge wasn’t theirs.

Digital wallets don’t remove the need for sound payment discipline. Disclosures, consent, audit trails, merchant classification — all of it still matters. But they give the consumer a familiar, fast experience while strengthening the underlying transaction. That combination is genuinely hard to find in this space.

The conversion case in collections

The most expensive friction in collections happens at the final step.

By the time a consumer is on a payment screen, every dollar and hour the agency invested in reaching that moment — outreach, segmentation, messaging, settlement structuring — is already spent. If the payment experience adds friction right there at the end, that investment evaporates.

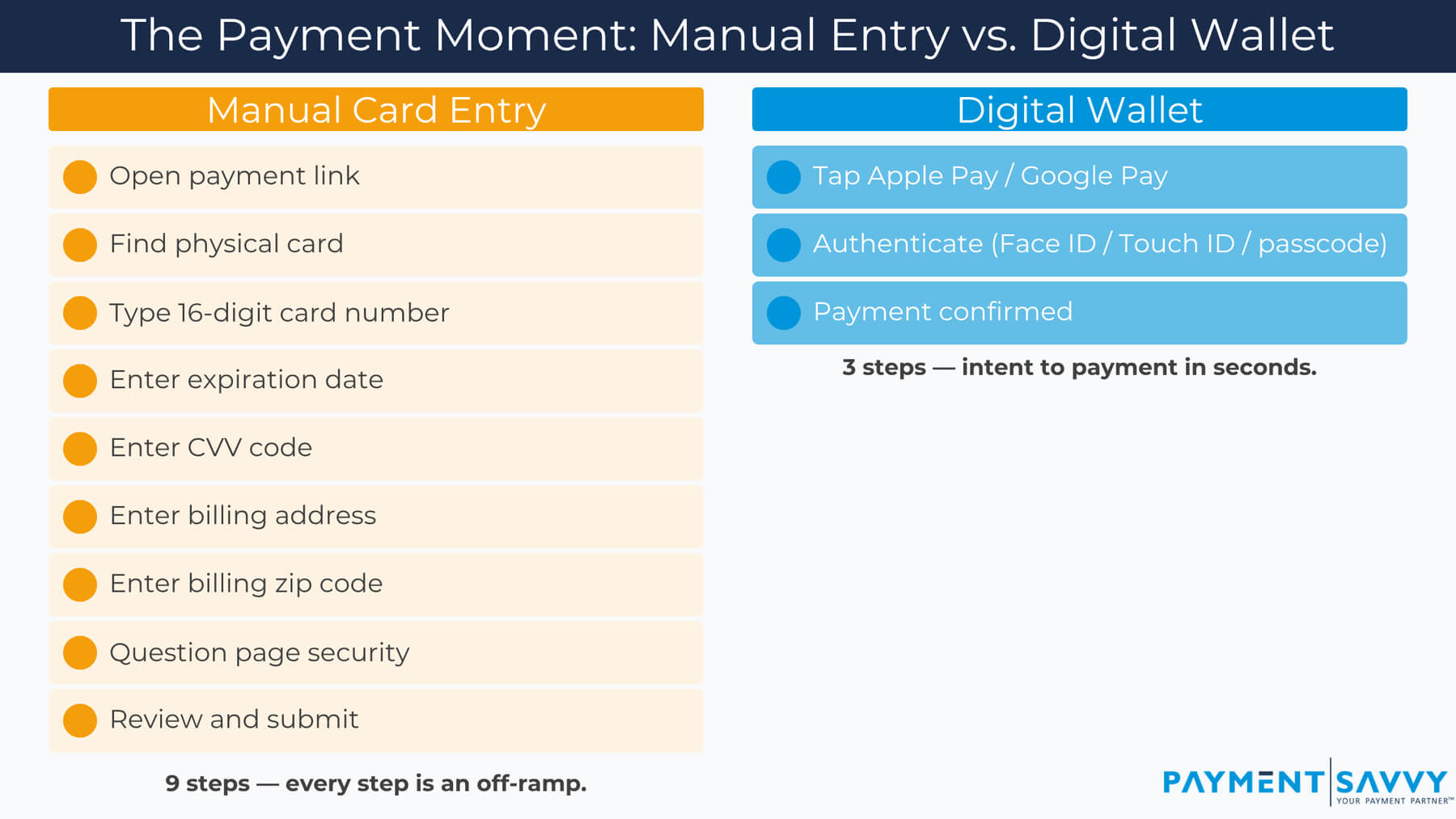

Manual card entry on mobile is where intent most often goes to die.

Consumers reaching for their physical card, fumbling a billing address, second-guessing whether the page is actually secure — every small step is an off-ramp. Stripe’s conversion data, Baymard’s research on mobile abandonment, and PayNearMe’s lending data all point to the same conclusion: wallets close that gap materially.

Industry estimates put completion uplift on payment plans and settlements in the 20 to 40 percent range when wallets are enabled. Even at the conservative end of that range, for an agency measuring recovery across portfolios where single-digit conversion shifts move material revenue, that’s not a rounding error. The conversion case isn’t theoretical. It shows up where collections actually keeps score.

Why collections specifically benefits

Here’s what actually happens with consumer intent in collections that doesn’t happen in retail: it’s fragile.

A consumer who’s decided to resolve a balance is often acting on a brief, emotionally charged window of readiness. The longer the payment process takes — the more cognitive load it carries — the higher the probability they pause, get distracted, or decide to come back later. And “later” in collections usually means never.

The shift toward mobile compounds this. Industry estimates put mobile share of bill payments at 50 percent and growing. KUBRA’s 2025 research shows that even among consumers who already use digital wallets elsewhere, many are simply unaware their billers offer the option — which means the opportunity gap isn’t just about willingness, it’s about awareness. That’s a solvable problem.

Wallets also support the flows collections actually depends on — not just one-time payments. Recurring arrangements, scheduled payments, settlements, payment plans: all of these benefit from saved, tokenized payment methods that don’t ask the consumer to re-enter card information each time. Payment durability — whether plans actually complete — improves when the payment method itself removes friction from the equation.

The case for digital wallets in collections isn’t about chasing a trend. It’s about recognizing that the structural conditions of this industry — fragile consumer intent, mobile-dominant engagement, recurring payment flows — happen to be exactly the conditions where wallets perform best.

What modernizing actually looks like

Let me be direct: adopting digital wallets isn’t a matter of dropping a button onto a payment page.

Done well, it’s a thoughtful re-evaluation of the payment flow itself. The first decision is use case. Wallets behave differently in one-time payments than they do in settlements, payment plans, recurring arrangements, or saved-credential flows. Each has different operational, authorization, and disclosure considerations. The right starting point is clarity on which flows the wallet is meant to support — not a broad “let’s turn it on” directive.

The second decision is infrastructure. Not every gateway or processor handles wallet transactions the same way. Some support wallets only for one-time card-not-present transactions. Others support the full range of recurring and saved-credential scenarios that collections depends on. Getting this right means choosing the right partner and configuration — not just enabling a feature.

The third decision is compliance flow. In collections, the payment button is one piece of a broader experience that must include disclosures, consent language, receipts, audit trails, and internal reporting. Wallets don’t change those requirements. They sit inside them.

Done thoughtfully, digital wallets in collections can become a real conversion lever. Done carelessly, they become a cosmetic feature that doesn’t move the numbers that matter.

Where Payment Savvy fits

At Payment Savvy, we work with collection agencies and high-risk merchants on exactly this kind of modernization — helping operators move beyond standard card-and-ACH flows into experiences that match how consumers already pay everywhere else.

Our platform supports Apple Pay and Google Pay across the flows agencies actually use: one-time payments, settlements, scheduled payments, recurring arrangements, payment plans. The goal isn’t to check a box on modern payment options. It’s to reduce friction at the final step of the consumer journey, where every percentage point of conversion compounds into measurable recovery.

If you’re evaluating how to bring digital wallets into your collections flow — or thinking more broadly about modernizing the consumer payment experience — we’d welcome the conversation.

The payment moment deserves the same attention as the rest of the journey

Meeting consumers where they already pay is no longer a stretch goal in collections. In every other industry competing for consumer attention and intent, it’s the baseline.

The payment moment is the finish line of the collections process. After all the work an agency has done to bring a consumer to that point, the experience they encounter there should reflect the world they actually live in — not the form fields and friction of a decade ago.

That’s the case for digital wallets in collections. Not because it’s coming. Because it’s already here.