What Is a Convenience Fee & Should You Charge It?

TABLE OF CONTENTS

Plenty of business owners run into this term long before they understand it. A customer calls to pay by phone, sees an extra charge tacked on, and asks what it’s for. Either way, you end up here.

Quick Facts

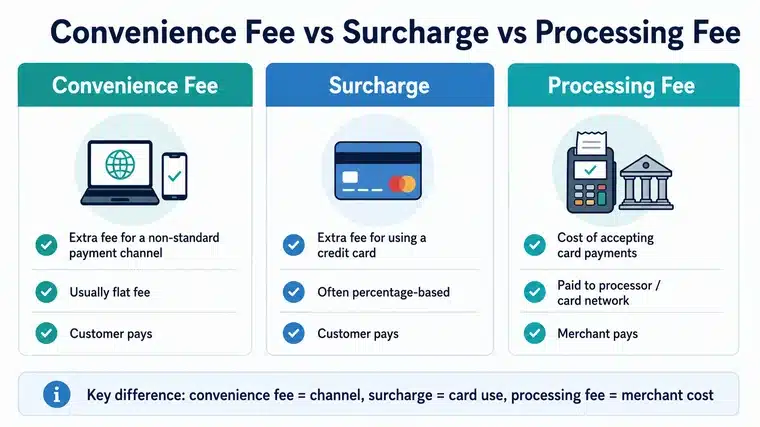

- A convenience fee is a flat charge added when a customer pays through a non-standard channel, like phone or online, instead of your normal payment method.

- It’s different from a surcharge, which applies specifically to credit card use and can be percentage-based.

- Convenience fees must be disclosed before the transaction completes, and a fee-free standard option has to exist alongside them.

- Visa requires the fee to be flat and generally won’t allow it on in-person or recurring transactions. Mastercard’s general rule is similar, aside from a narrower government/education program.

- Convenience fees are legal across the U.S., though a handful of states warrant a closer look first.

- Businesses can offset card costs without the “fee” label entirely, through cash discounting or by steering customers toward ACH.

Understanding the Convenience Fee Meaning

Defining Convenience Fees for Modern Merchants

So what is a convenience fee, exactly? It’s an extra charge added to a transaction when a customer chooses a payment method outside your business’s normal channel.

A quick example: a brick-and-mortar shop that takes cash and in-person cards starts accepting payments over the phone. That phone payment is the “non-standard” channel. The convenience fee meaning hinges entirely on that contrast: there has to be a standard way to pay, and the fee only applies to the alternative.

This is the convenience fee definition that card networks actually enforce, not just a marketing term. Charge a fee where no real alternative exists, and you’re not running a convenience fee program; you’re running a violation waiting to get flagged.

Why Businesses Use an Online Convenience Fee

Processing a card payment costs money: interchange, network fees, and your processor’s markup. An online convenience fee lets you offer that payment option without eating the cost yourself. The customer who wants the speed of paying online, or the flexibility of paying by phone at 11pm, covers the expense of providing that option.

It’s cost recovery, not free money, tied to a specific service you’re providing beyond your baseline operations. Done right, it lets you say yes to more payment methods without your margins taking the hit every time someone reaches for a card instead of a check.

Convenience Fee vs. Surcharge: Critical Differences

People use these terms interchangeably, and that’s exactly where businesses get into trouble. They are not the same thing, and the rules that govern them are not the same either.

The Product vs. The Channel: Where the Fee Applies

A surcharge attaches to the card itself. It doesn’t matter how the customer is paying, in person, online, or by phone: if they’re using a credit card, the surcharge applies. A convenience fee attaches to the channel instead. It’s charged because the customer used an alternative way to pay, regardless of which specific card they used within that channel.

This distinction is the whole legal foundation for convenience fees. You can’t charge one if your business only operates online, because there’s no standard channel for the online option to be an alternative to.

Percentage vs. Flat Fee Structures

Surcharges are commonly percentage-based, a cut of the transaction total. Convenience fees, under Visa’s rules, have to be flat. A $5 fee for paying online is fine. A 3% fee for paying online runs into trouble, and Mastercard’s general rule for most merchants is no more forgiving on that point.

Comparison Table: Surcharge vs. Convenience Fee

| Surcharge | Convenience Fee | |

| Applies to | Credit card use, any channel | Non-standard payment channel |

| Fee structure | Often percentage-based | Must be flat (Visa) |

| Requires alternative? | Must offer non-card option | Must offer standard, fee-free channel |

| State restrictions | Banned or capped in several states | Legal nationwide, with regional caveats |

| Recurring payments | Generally allowed where legal | Generally not permitted, with narrow exceptions |

Convenience Fee vs. Processing Fee: Who Pays What?

Understanding Interchange and Merchant Service Fees

A processing fee, sometimes called a merchant service fee, is what you pay your processor and the card networks for the privilege of accepting cards at all. Interchange goes to the issuing bank, assessment fees go to the network, and your processor takes its own cut on top. None of that comes from the customer. It comes out of your revenue, transaction by transaction.

A convenience fee vs processing fee comparison comes down to direction. Processing fees flow from you to the people who make card acceptance possible. Convenience fees flow from the customer to you, specifically to offset the processing fees tied to that one transaction.

How Convenience Fees Offset Your Overhead

When it’s working properly, a convenience fee program means you’re not absorbing the cost of offering an extra payment channel out of your own margins. The customer pays it, you pass it straight through to cover what the card network and your processor are charging you, and your revenue on the underlying transaction stays intact. The fee isn’t profit. It’s a wash, by design.

Major Card Network Rules: Visa, Mastercard, and Beyond

Every network has its own take on what’s allowed.

Visa’s Strict “Alternative Channel” Requirements

Visa is the strictest of the major networks. A few hard rules:

- The fee has to be flat, never a percentage.

- It must apply equally across every alternative payment type you offer. You can’t charge $5 for phone payments and $2 for online ones.

- It can only be charged on a genuine alternative channel, never your business’s primary, in-person payment method, and generally not on recurring or installment payments either.

Mastercard’s General Rule vs. Its Government and Education Program

Mastercard’s baseline rule for most merchants tracks Visa closely: the fee has to apply equally across payment methods, and it generally can’t be tacked onto recurring payments either.

Where Mastercard genuinely differs is a separate, narrower track: the Mastercard Government/Education Convenience Fee Program, open only to pre-certified government and education entities. Within that program Mastercard allows more flexibility, including in-person transactions. It’s not a general merchant allowance.

American Express and Discover: The “Equal Treatment” Rule

Amex doesn’t publish as detailed a convenience fee policy as Visa, but its merchant rules are actually a bit more permissive in one respect: Amex allows convenience fees on recurring and installment transactions, where Visa generally doesn’t.

The core requirement stays the same: the fee has to fit the genuine convenience fee definition, apply equally across payment methods, and be disclosed upfront.

Discover doesn’t publish its own detailed convenience fee rulebook the way Visa does, but it requires equal treatment across card types too. No favoring one network’s customers with a lower fee than another’s.

The common thread across every network: consistency. Pick a fee, apply it the same way to every alternative channel, every time.

Legal Restrictions: Can You Legally Charge a Convenience Fee?

This is where the conversation gets murky, mostly because people conflate convenience fees with surcharges. They are not regulated the same way. Businesses that don’t separate the two end up making compliance decisions based on the wrong law.

Where Surcharges Face Real Restrictions

Surcharges, the percentage-based card fees, are the ones running into state-level bans and caps. A small number of states still prohibit them outright, and a few more cap the percentage or tie it strictly to the merchant’s actual cost of acceptance. The legal landscape here has shifted repeatedly as court challenges have struck down some bans while others remain enforced.

Check the current law in every state where you operate before flipping on a surcharge program.

Convenience Fees: Legal Nationwide, With a Few Caveats

Convenience fees sit in a different legal category. They’re broadly legal across the country, including in states where surcharges are banned, because they’re structured around offering an alternative channel rather than penalizing card use directly.

That said, “legal nationwide” doesn’t mean “identical everywhere.” A handful of states have their own specific rules for convenience fees on top of the card network requirements, and some of the state-level caution floating around for convenience fees is actually a surcharge law that some processors interpret broadly enough to sweep convenience fees in too.

The details shift often enough, and the consequences of getting it wrong are real enough, that this is genuinely worth a quick check with a local attorney or your payment processor before launching a program, rather than assuming a general nationwide answer covers your specific state.

Federal Regulations and Disclosure Requirements

There’s no single federal law that regulates convenience fees directly. What does apply everywhere is disclosure: the fee has to be clearly communicated before the customer completes the transaction, with no exceptions buried in fine print.

Pros and Cons of Implementing Convenience Fees

The Benefits

- Offsets processing costs. You stop absorbing the expense of accepting cards through an alternative channel.

- Encourages lower-cost payment methods. Customers who want to avoid the fee often shift to ACH or other no-fee options, which cost you less to process anyway.

- Makes costs transparent. Customers see exactly what they’re paying for instead of it getting buried in your base pricing.

The Risks

- Customer friction. Some customers see any added fee as a reason to look elsewhere, especially if competitors don’t charge one.

- Implementation complexity. Card network rules, plus state-level nuance around surcharges bleeding into convenience fee territory, make this harder to set up correctly than it looks.

- Pricing perception. Even a flat, well-disclosed fee changes how customers perceive your overall cost, and that perception doesn’t always work in your favor.

Industry Use Cases: When Fees Make Sense

Government Agencies and Educational Institutions

Government offices and schools are some of the most natural fits for convenience fee programs. Citizens paying permit fees, fines, or tuition online instead of mailing a check are using a genuine alternative channel, exactly the scenario convenience fees were built for. Payment Savvy’s government and non-profit payment processing and school payment processing solutions are both built around this kind of channel-based structure.

Healthcare Practices and Medical Billing

Healthcare billing runs into convenience fees constantly, particularly around patient portals and phone-based payments for copays and outstanding balances. The standard channel is often paying in-office or by mail; an online portal or call center payment can carry a disclosed convenience fee on top. Payment Savvy’s healthcare payment processing solutions are designed around exactly this kind of billing flexibility.

Specialized and High-Risk E-commerce Businesses

E-commerce is trickier territory. If your business operates entirely online, there’s no standard, non-online channel for a convenience fee to apply against, so the model often doesn’t fit. Where it does show up is in specialized or high-risk merchant categories that combine phone orders with web sales, where the phone channel can carry a fee the web channel doesn’t.

How to Legally Implement Fees: A Merchant’s Checklist

Getting this right isn’t complicated, but skipping a step is how merchants end up with a card network compliance issue months later.

- Confirm a “bona fide” alternative channel exists. You need a genuine non-standard way of paying, distinct from your normal operations, for the fee to apply to.

- Disclose the fee before the transaction finalizes. Customers need to see it and have the chance to back out or switch payment methods before they commit.

- Keep a standard, no-fee option available. Whether that’s in-person payment, mail-in checks, or ACH electronic transfers, customers need a way to pay without the fee.

- Set a fixed, flat rate. Visa requires this. Don’t build a percentage-based structure and assume it’ll pass network review.

Skip any one of these, and you’re not running a compliant convenience fee program, you’re running a surcharge with a different name on it.

Smart Alternatives to Protect Your Revenue

Cash Discounting Programs: A Positive Reinforcement Model

Cash discounting flips the convenience fee model on its head. Instead of charging more for card payments, you build the processing cost into your base price and offer a discount to customers who pay by cash or another lower-cost method. The revenue impact is similar either way. Psychologically, it lands completely differently: nobody resents a discount the way they resent a fee.

Integrating Fees into Base Product Pricing

The simplest option, with zero compliance overhead: build your card acceptance costs into your prices across the board. No fee to disclose, no alternative channel requirement, no card network rulebook to track.

Promoting ACH Transfers and Digital Wallets

Steering customers toward ACH does double duty. It avoids convenience fee and surcharge questions entirely since there’s no card involved, and it costs less to process than a card transaction in the first place.

Payment Savvy’s ACH payment processing runs at a fraction of typical card processing costs, which makes it worth promoting as the default option rather than an afterthought.

Maximizing Profit With Payment Savvy’s Fee-Free Payments™

Running a compliant convenience fee program takes more than deciding to add a charge. You need the right channel distinction, the right disclosure flow, and a fee structure that holds up under whichever card networks your customers use. Payment Savvy’s Fee-Free Payments™ program handles that structure for you:

- Customers choosing card payment see the disclosed fee before they complete the transaction.

- ACH electronic check payments stay fee-free as your standard alternative.

- Your team isn’t manually tracking Visa’s and Mastercard’s flat-fee and recurring-payment restrictions every time something changes.

For businesses operating in high-risk categories, the fee structure question gets more complicated, not less. Payment Savvy builds custom gateway solutions that account for both the elevated risk profile and the channel-based compliance requirements these merchants face.

Get a Compliant Convenience Fee Program Set Up

A convenience fee can do exactly what it’s meant to: let you offer customers more ways to pay without absorbing the processing cost yourself. But the model only works if there’s a real distinction between your standard channel and the alternative one you’re charging for. Blur that line, or skip the disclosure step, and you’ve built a compliance problem instead of a cost-recovery tool.

Payment Savvy’s convenience fee processing solution is built around exactly those requirements: a genuine channel distinction, automatic disclosure, and a flat fee structure that holds up under Visa and Mastercard rules alike. If you’re ready to stop absorbing card processing costs without risking a compliance headache, that’s the place to start.

Frequently Asked Questions

What does convenience fee mean on a bill?

It means you were charged extra for using a payment channel outside the business’s standard method, typically paying online or by phone instead of in person or by mail. It should be itemized separately and disclosed before you completed the payment.

Can I charge a convenience fee for in-person credit card payments?

Generally no. A fee charged specifically because a customer used a credit card, regardless of channel, is a surcharge, not a convenience fee. Convenience fees are tied to an alternative payment channel, like phone or online, not to the card itself. If your standard channel is already in-person, you can’t charge a convenience fee for staying in that same channel.

Are online convenience fees legal in Texas?

Yes. Texas law restricts credit card surcharges specifically, and that restriction is itself tangled up in ongoing court rulings. Convenience fees are a separate category and are explicitly permitted under Texas law regardless of how the surcharge question eventually settles, as long as the fee meets the standard requirements: a genuine alternative channel, flat structure, and clear disclosure.

Is a convenience fee refundable if I return an item?

It depends on the merchant’s policy, and card network rules don’t mandate a refund either way. Many businesses don’t refund the convenience fee even when the underlying purchase is refunded, since the fee covered the cost of processing the original transaction regardless of the outcome. Check the specific merchant’s terms, since this varies.